Protecting Deposits

Promoting Stability in Bermuda’s Financial System

Enhancing Bermuda’s Attractiveness as a World-Class Financial Jurisdiction

Strengthening Bermuda’s Financial Safety Net

What is Deposit Insurance?

Deposit insurance is a scheme to protect deposits held with a Scheme Member, whereby eligible depositors will be compensated up to a maximum specified amount of their deposits upon failure of that Scheme Member.

The primary function of a deposit insurance scheme is to provide protection for deposits in the event that an individual Scheme Member becomes insolvent or encounters other problems that threaten its survival. A well-structured deposit insurance scheme can also help to bolster public confidence and thereby help to reduce the risk of problems with one Scheme Member escalating into a crisis or spreading to other Scheme Members.

Deposit insurance should be viewed as an integral part of the arrangements for deposit protection in Bermuda. The implementation of a sound deposit insurance scheme, coupled with a prudent and effective regulatory and supervisory framework, strengthens the financial safety net in Bermuda.

The Deposit Insurance Scheme in Bermuda

The framework for the Bermuda Deposit Insurance Scheme (the “Scheme”) was established by the Deposit Insurance Act 2011 (the “Act”) and the Deposit Insurance Rules 2016 (the “Rules”). The Act defines the establishment, functions and basic operations of the Scheme and provides that the Scheme be administered by the BDIC. A Scheme Member is defined in the Act as any bank or credit union that is licensed by the Bermuda Monetary Authority (the “Authority“).

The operation of the Act is governed by the Rules.

The Deposit Insurance Scheme has three main objectives:

Deposit insurance offers protection to the deposits of eligible depositors, who are within scope of the Scheme, against losing all of their money deposited with that Scheme Member should it fail.

The protection of deposits and the stability of the financial system are inter-related to the extent that stability is influenced by the degree of confidence depositors have in the system and their willingness to keep funds on deposit. Any loss of deposits held at a Scheme Member by depositors may result in a fall in local consumption, and a loss of public confidence may lead depositors to transfer monies to other countries. The Scheme helps to prevent this.

Public confidence reduces the likelihood that depositors with an individual Scheme Member panic and withdraw funds suddenly if concerns arise about the condition of that Scheme Member. We have seen examples outside of Bermuda where concerns about one financial institution have at times led to concerns about others, resulting in so-called “contagion runs”. Thus, deposit insurance supports the stability and smooth operations of the entire financial system by providing timely access to insured depositors’ funds. Delays in access can also cause financial hardship for depositors, who may need funds for everyday living expenses. A deposit insurance scheme that provides prompt access to funds aids in enhancing public confidence in Bermuda’s financial system.

In a world that looks to regulation and insurance as a way of gauging the stability and security of the financial environment in any given country, the Scheme enhances Bermuda’s attractiveness and reputation as a well-regulated financial jurisdiction. In the absence of a lender of last resort, the oversight provided by the Bermuda Monetary Authority, which oversees the operation of a mature and highly regarded regulatory system over the Island’s financial institutions, and the protection offered by the Scheme, are seen as vital to creating an enhanced financial safety net in Bermuda.

DEPOSIT

INSURANCE

ACT 2011

Why Do We Need Deposit Insurance?

The global financial crisis of 2008 caused regulators around the world to re-evaluate existing regulatory and institutional frameworks. The incidence of significant losses on the part of financial institutions globally led to heightened interest on the part of the general public, policy makers and regulators in the key aspects of the financial safety net.

In Short

- The Scheme has a narrow mandate separate from but in addition to the supervisory role of the Bermuda Monetary Authority.

- Participation in the Scheme is mandatory for all Scheme Members. Scheme Members are defined in the Act as any bank or credit union that is licensed by the Authority. A list of Scheme Members can be found [AnythingPopup id=”3″].

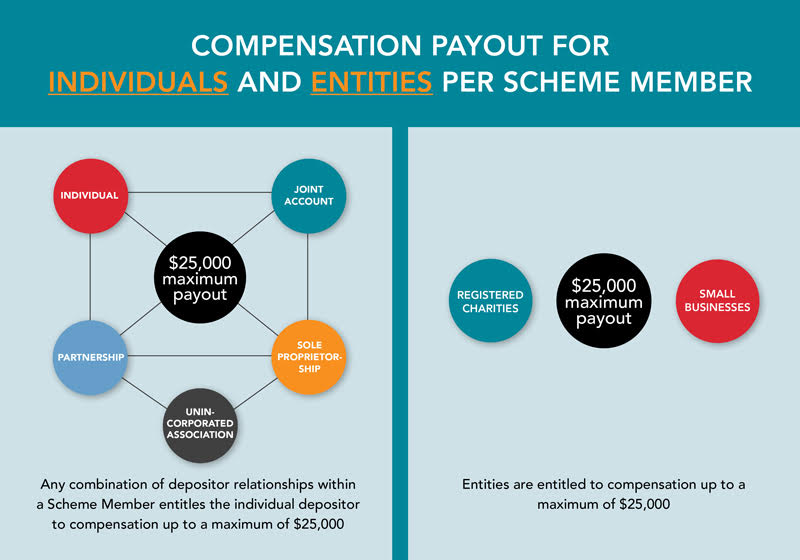

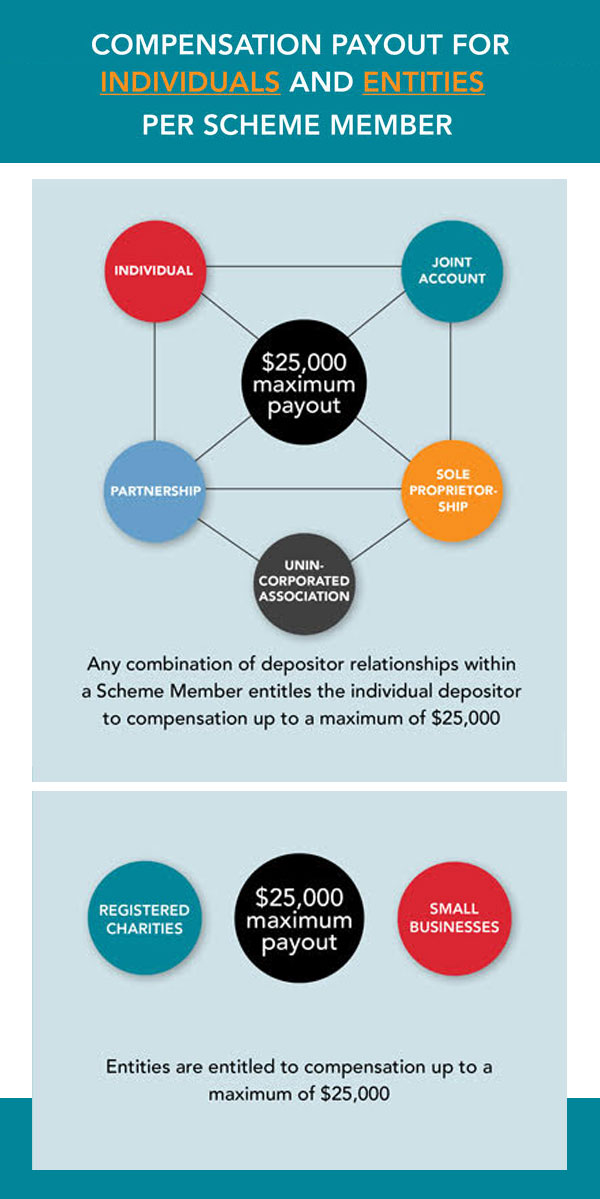

- The coverage amount of the Scheme has been set up to a maximum of $25,000 per insured depositor, per Scheme Member.

- The Scheme covers Bermuda Dollar deposits held by insured depositors at Scheme Members. Insured depositors include individual and joint account holders, individuals that hold accounts in the name of sole proprietorships, partnerships, and/or unincorporated associations, as well as charities registered under the Charities Act 1978 and companies registered in the Register of Small Businesses maintained by the Bermuda Economic Development Corporation (BEDC).

- The Scheme is funded by premiums paid to the BDIC by Scheme Members.

- The Scheme is a domestic insurance scheme. It does not cover deposits held in overseas subsidiaries or branches of Scheme Members. Neither does it cover foreign currency deposits in accounts with Scheme Members for depositors.

Costs of Deposit Insurance

Deposit insurance is not without cost. In the first instance, there is the collection of premiums for funding the Scheme and to enable the payment of compensation up to a maximum of $25,000 per insured depositor.

With a coverage level of $25,000, and at current premium rates, the direct cost is likely to be in the order of $6 million to $7 million a year.

In addition to the direct funding costs, there will be the costs of administering the Scheme itself, which the BDIC intends to keep as low as possible. There will also be certain indirect costs associated with the introduction of the Scheme, such as the Bermuda Government providing liquidity support to the Scheme while the Deposit Insurance Fund (the “Fund”) is being built up.

Membership and Coverage

Compulsory participation of all qualifying financial institutions in a deposit insurance scheme is the practice usually adopted internationally. This is to promote comprehensive protection to deposits and to avoid adverse selection, which might give rise to instability in the financial system. Accordingly, it has been legislated that participation in the Scheme is mandatory for all banks and credit unions as outlined in Section 11 of the Act. Scheme Members are defined in the Act as any bank or credit union that is licensed by the Authority.

It has been established that those persons protected by the Scheme comprise the following:

- Individuals

- Individuals in respect of joint accounts

- Individuals who place a deposit in an account with a Scheme Member in the name of a:

- Sole proprietorships

- Partnerships

- Unincorporated association

- Charities registered under the Charities Act 1978

- Companies registered in the Register of Small Businesses maintained by the BEDC

It has further been established that the following Bermuda Dollar deposits are eligible for protection under the Scheme:

- A deposit in a savings account

- A deposit in a fixed deposit account

- A deposit in a current (chequing) account

- A deposit in a credit union member’s share account

About Us

The BDIC is an independent statutory corporation, headed by a Board of Directors. The Board of Directors consists of a Chairman, the Chief Executive Officer, the Chief Executive Officer of the Authority, the officer of the Bermuda Monetary Authority responsible for the supervision of Scheme Members, the Financial Secretary and not less than two and not more than four other directors. The Minister of Finance appoints the Chairman and other directors of the BDIC from amongst persons with proven experience in banking or financial services.

Functions of the BDIC

In the management of the Scheme, the BDIC exercises the following principal functions:

- Collects premiums from Scheme Members;

- Assesses claims made against the Scheme and determines the eligibility and entitlement of claimants;

- Makes compensation payments to insured depositors as determined under the Act;

- Recovers any amount paid out to a failed Scheme Member’s insured depositors from the assets of the failed Scheme Member; and

- Educates the public on matters relating to the Scheme.

Deposit Insurance Premiums

Premiums collected by the BDIC from Scheme Members will only be used for:

- Payment of compensation to insured depositors;

- Payment of principal and interest on any borrowings by the BDIC;

- Purchase of permitted investments by the BDIC; and

- Payment of administrative costs of the BDIC.

Premiums collected by the BDIC are held in a fiduciary capacity for the insured depositors in case of the failure of a Scheme Member. To reflect this trust, the investment guidelines emphasise “safety and liquidity” over “return”.

Deposit Insurance Funding

In order for a deposit insurance scheme to be well-structured and effective, it must have ready access to adequate funds to ensure prompt payment of compensation to insured depositors.

A number of options are available for collecting premiums to be put into a deposit insurance fund. Contributions may be levied up front to build up a deposit insurance fund (pre-funded), or after a member failure (post-funded) or a combination of both. Post-funding provides finance to a deposit insurance fund after a member fails. While this method requires less administrative, maintenance and funding costs, funding requirements may impose a financial burden on the system as the need to pay assessments or levies to deal with failures occurs at an inopportune time. Thus, most countries favour some form of pre-funded scheme. Pre-funding uses periodic contributions by member institutions to build up resources for the payment of compensation to insured depositors in the case of a Scheme Member failure. This ensures that a liquid pool will be readily available to make quick payments to insured depositors, reduces the need for cross-subsidisation (i.e. financial burden being absorbed by surviving members) and helps reinforce public confidence in such schemes.

Bermuda’s Deposit Insurance Scheme is pre-funded by premiums paid to the BDIC by Scheme Members. These are paid on a quarterly basis and are calculated on a percentage rate basis with reference to the amount of insured deposits held by an individual Scheme Member. The percentage rate chargeable is currently set at 0.25% per annum of the Scheme Member’s insured deposits. These premiums are accumulated in the Fund.

Board of Directors

The BDIC is governed by a Board of Directors. The Board of Directors is responsible for the proper administration and management of the Scheme and the Fund. In order for the BDIC to discharge its functions effectively, the Board of Directors has the necessary powers to finance compensation payments, borrow where necessary to ensure prompt reimbursement to insured depositors, enter into contracts, invest the Scheme premiums in the manner specified in the Act, set internal operating budgets and procedures, obtain information from Scheme Members and appoint agents or authorise third parties to perform any of the functions of the Board of Directors under the Act.

The current members of the BDIC Board of Directors are:

Stephen Todd, JP, CHAIRMAN, CEO, The Bermuda Hotel Association / Hotel Employers of Bermuda

Alan Richardson, CPA, CA, CEO, Bermuda Deposit Insurance Corporation

The Hon Maxwell Burgess, JP, Retired

Mark Crockwell, CFA, Treasurer, Said Holdings Ltd.

Ashley Kibblewhite, Director, Banking, Trust, Corporate Services & Investment, Bermuda Monetary Authority

Nathan Kowalski, CPA, CA, CFA, CIM, CFO, Anchor Investment Management Ltd.

Chid Ofoego, Financial Secretary, Government of Bermuda

Tammy Richardson-Augustus, Partner, Appleby

Craig Swan, CEO and Executive Director, Bermuda Monetary Authority

BDIC and the Bermuda Monetary Authority

The Authority is responsible for the supervision of Scheme Members and the overall stability of the Bermuda banking system. The sole function of the BDIC is to protect insured deposits if a Scheme Member fails. The roles of the Authority and the BDIC complement each other in achieving the common objectives of protecting deposits and promoting stability in the financial system. Although the BDIC is independent of the Authority, an officer of the Authority responsible for the supervision of Scheme Members is also a member of the Board of the BDIC.

Public Access to Information (PATI)

The BDIC, as a statutory corporation, is required under the Public Access to Information Act 2010 (“PATI Act”) to publish an Information Statement, which is intended to help the public access information and records that we hold.

The PATI Act creates a new and welcomed culture of openness for public authorities within our country. It introduces the idea that records held by public authorities are a national resource for all of us and the BDIC wholeheartedly endorses this shift and we are committed to openness, good governance and transparency.

FAQs

If you require further information or clarification on any of these or other questions, please contact the BDIC office.

WHY IS DEPOSIT INSURANCE NECESSARY IN BERMUDA?

WHAT DOES DEPOSIT INSURANCE PROVIDE?

HOW WAS THE DEPOSIT INSURANCE SCHEME ESTABLISHED?

WHICH FINANCIAL INSTITUTIONS ARE PARTICIPATING IN THE DEPOSIT INSURANCE SCHEME?

HOW IS THE DEPOSIT INSURANCE SCHEME FUNDED?

HOW IS THE DEPOSIT INSURANCE FUND MANAGED AND WHERE ARE THE FUNDS HELD?

WHO IS AN INSURED DEPOSITOR?

- Individuals

- Individuals in respect of joint accounts

- Individuals who place a deposit in an account with a Scheme Member in the name of a:

- Sole proprietorships

- Partnerships

- Unincorporated association

- Charities registered under the Charities Act 1978

- Companies registered in the Register of Small Businesses maintained by the BEDC

WHAT IS AN INSURED DEPOSIT?

- A deposit in a savings account

- A deposit in a fixed deposit account

- A deposit in a current (chequing) account

- A deposit in a credit union member’s share account

Bermuda Dollar deposits that are pledged, charged or secured as collateral toward a borrowing are not protected under the Scheme.

IS THE DEPOSIT INSURANCE FUND SUFFICIENT TO COVER A SCHEME MEMBER'S FAILURE AND, IF NOT, WHEN WILL IT BE SUFFICIENT?

The ultimate determination of the size of the Fund necessary will have to be undertaken by carrying out an actuarial evaluation once sufficient data has been received from Scheme Members.

WHAT IS THE AMOUNT OF INSURANCE COVERAGE AND HOW DOES IT APPLY?

For example, Mr. Smith has three Bermuda Dollar accounts with a Scheme Member, each having a balance of $10,000. One account is a savings account, one is a current (chequing) account, and the other is a fixed-term deposit account. All of these accounts are insured deposits covered by the Scheme. If the Scheme Member where Mr. Smith’s accounts are held failed, Mr. Smith would be entitled to a compensation payment of $25,000 (the maximum allowed), even though his deposits totalled $30,000. On the other hand, if Mr. Smith’s accounts had a balance of $5,000 in each, he would only be entitled to a compensation payment of $15,000, representing the total insured deposits held in his accounts.

HOW ARE JOINT ACCOUNTS HANDLED?

For example, Mr. Smith and a friend, Ms. Jones, hold a Bermuda Dollar joint account with a balance of $20,000 at a Scheme Member. If the Scheme Member where Mr. Smith and Ms. Jones’ joint account is held fails, Mr. Smith and Ms. Jones would each be entitled to a compensation payment of $10,000. On the other hand, if the joint account balance is $60,000, Mr. Smith and Ms. Jones are each deemed to own $30,000 in the account and would each be entitled to a compensation payment up to a maximum of $25,000.

WHAT HAPPENS IF I HAVE AN INDIVIDUAL ACCOUNT AND A JOINT ACCOUNT?

WHAT HAPPENS IF I HOLD DEPOSIT ACCOUNTS IN MORE THAN ONE SCHEME MEMBER?

For example, Mr. Smith has $25,000 in a Bermuda Dollar savings account with Scheme Member A and $25,000 in a fixed-term Bermuda Dollar deposit account with Scheme Member B. If both Scheme Members fail, he will be entitled to a compensation payment up to a maximum of $25,000 in respect of the savings account and $25,000 in respect of the fixed-term deposit.

On the other hand, if Ms. Jones has $10,000 in a Bermuda Dollar current (chequing) account with Scheme Member C and $50,000 in a fixed-term Bermuda Dollar deposit account with Scheme Member D, she will be entitled to a compensation payment of $10,000 in respect of the current (chequing) account and up to a maximum of $25,000 in respect of the fixed-term deposit.

WHAT HAPPENS IF I HAVE A DEPOSIT ACCOUNT AND A LOAN OR OTHER LIABILITY WITH A SCHEME MEMBER?

For example, if Mr. Smith has $50,000 in his Bermuda Dollar deposit account and holds an unpaid balance of a bank loan in the amount of $15,000 (in any currency and with the same Scheme Member), the net balance remaining in his favour is $35,000. He will therefore be entitled to a maximum compensation payment of up to $25,000.

On the other hand, if Ms. Jones has a total of $50,000 in her Bermuda Dollar deposit account and an unpaid balance of a bank loan in the amount of $60,000 (in any currency and with the same Scheme Member), there is a negative balance attributable to Ms. Jones, and she will therefore not be eligible for any compensation payment.

HOW ARE COMPENSATION PAYMENTS HANDLED FOR SOLE PROPRIETORSHIPS, PARTNERSHIPS, AND/OR UNINCORPORATED ASSOCIATIONS HANDLED?

An example of how a sole proprietorship would be handled is if Ms. Jones has $30,000 in a personal Bermuda Dollar current (chequing) account and another $60,000 in a Bermuda Dollar account set up for her sole proprietorship business. In this instance, she would be entitled to a maximum compensation payment up to $25,000 for the two accounts.

ARE ALL SMALL BUSINESSES COVERED?

WHAT HAPPENS IF I HAVE AN INDIVIDUAL ACCOUNT AND I ALSO OPERATE A COMPANY REGISTERED AS A SMALL BUSINESS WITH THE BEDC, WHICH HAS ITS OWN ACCOUNT?

ARE ANY TYPES OF DEPOSITS EXCLUDED FROM COVERAGE?

For example, Ms. Jones has a Bermuda Dollar current (chequing) account with a balance of $15,000 and a US Dollar fixed-term deposit account with a balance of $20,000. In the event of the Scheme Member’s failure, Ms. Jones will only be entitled to a compensation payment on the Bermuda Dollar account balance up to $15,000. She will not be entitled to any compensation for the US Dollar account.